in the belly of the healthcare beast

dissecting Mark Ruffalo's recent healthcare take

I spent the better part of this week navigating America’s healthcare system — somewhere between awe at the mechanics of keeping up with seemingly endless demand and total frustration with overrun emergency rooms and endlessly delayed timelines.

In the middle of it, I came across this post from Mark Ruffalo. Ruffalo is no stranger to sweeping statements about the state of our nation, often emotionally charged, usually directionally right. This one felt worthy of going deeper on given the context.

So I applied the framework you’re used to reading every Friday for myself. Here’s how it played out.

the mechanism underneath: how health insurance works

Health insurance works by pooling risk. A lot of people pay into a big pool, a smaller number draw out when they’re sick, and the bigger pool covers those costs.

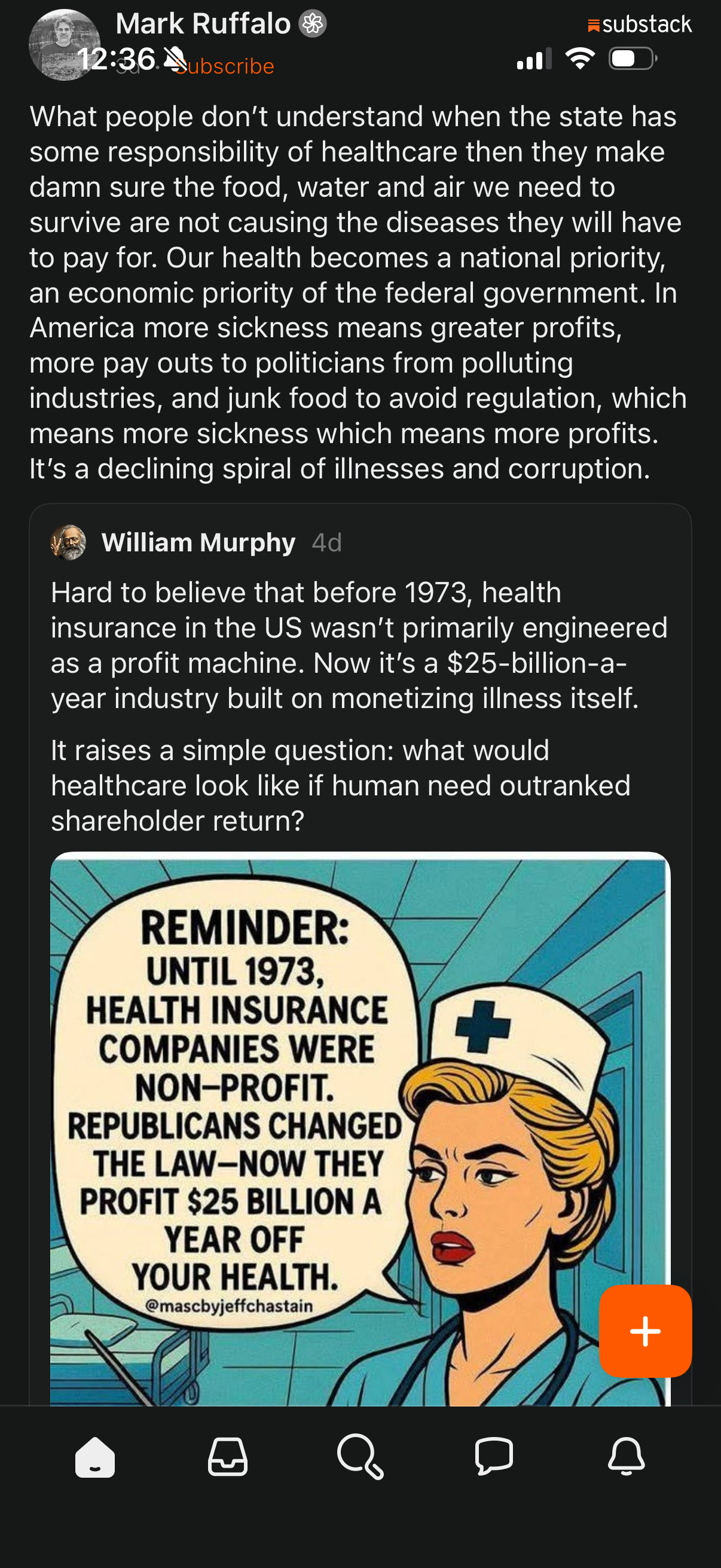

Before the 1970s, most health insurers were nonprofits. They ran on a simple mandate: everyone in the pool pays roughly the same premium (monthly payment to keep insurance active) whether they’re sick or healthy, young or old.

The 1973 HMO Act required employers to offer lower-cost, more tightly controlled health plans alongside traditional coverage for the first time. For investors, that was the signal they needed; a federal law had just made healthcare a viable market. Money poured in.

But the bigger structural shift came in the 1990s, when competitive pressure pushed several major nonprofit Blue Cross Blue Shield plans to convert to for-profit status themselves.

Why? For-profit insurers could do something nonprofits couldn’t: they could raise capital by selling stock, and cherry-pick customers, insuring younger, healthier people and avoiding sicker ones.

Nonprofits were still covering everyone at the same rate, which meant their pools were getting older and sicker while the competition’s pools were getting younger and healthier.

The math eventually became unsustainable. Several major Blue Cross Blue Shield plans concluded that the only way to survive was to convert to for-profit and operate like a business. So off they went.

The ownership structure of health insurers sounds boring, but here’s why it matters: a nonprofit’s legal obligation is to its mission. A for-profit’s is to its shareholders. In some industries, those two things can coexist (profit and mission), but in insurance, they create a direct conflict.

When your business model rewards paying out less than you take in, the pressure to find reasons to deny claims, delay approvals, and limit which doctors patients can see is incentivized.

Back to Ruffalo’s post.

the nuance

Ruffalo’s argument is emotionally compelling but analytically thin.

The post correctly identifies a real structural problem: the profit motive is misaligned with health outcomes for patients. But the “one party’s law did this” framing squeezes a 50-year, bipartisan story into an oversimplified take.

For-profit insurers existed before 1973. The HMO Act didn’t create them for the first time, but rather just opened a door. The bigger trigger came in 1994, when the Blue Cross Blue Shield Association changed its own rules to allow member plans to convert to for-profit status. Several did, starting with Blue Cross of California. What followed was a wave of conversions driven by competitive pressure, not a single law passed by a single party.

So, the structural critique is legitimate, but the facts aren’t totally there.

Insurance is a uniquely bad fit for traditional market logic, but fixing ownership won’t fix the cost.

In most industries, you profit by giving customers more of what they want. In health insurance, you can profit by giving them less. That’s the structural problem here. But fixating on insurer ownership obscures the bigger driver: what hospitals and doctors actually charge. American providers charge 2x more than peer countries for the same procedures — because local hospital monopolies set prices without competition, doctors get paid per visit, not per outcome, and nobody negotiates rates nationally the way other governments do.

Nonprofit structures also failed, they just failed differently.

Before for-profit dominance, nonprofits weren’t denying care based on cost, but they were still denying care.

Slow approvals, narrow coverage, and administrative gatekeeping were all at play. In that way, the limiting mechanism was bureaucracy instead of a financial incentive, but the outcome for the patient could look similar. Government-run healthcare has its own questionable track record, too: VA wait time crises and Medicaid reimbursement rates being so low that many providers won’t even accept it.

So the honest debate becomes more about which accountability mechanism you trust more: markets, government, or some hybrid.

the real question

Is healthcare a commodity best allocated by markets, or a public good, best guaranteed by collective structures? That’s the question the meme never asks (they never do), and it’s a certified toughie.

what this means for you

I’m of the mind that healthcare should act in the service of people’s health, not business interests. Period. Ruffalo noting the dynamic of us being in good health not being the point of the system right now lands well with me.

But, though it’d be easy for me to say it’s all the profit motive’s fault, that doesn’t cover the full story, either. These things are never as simple as the 140-character version.

The profit motive is most dangerous when the entity profiting is the one deciding whether you get care. But upstream of that (in research, drug development, or medical technology) the profit motive has driven real breakthroughs that government-run systems may not have.

The policy answer you land on depends entirely on what you think the role of government is. It’s a values question. It’s about individual vs. collective responsibility, about what we owe each other as citizens, and about whether healthcare is more like a fire department (public good, everyone gets it) or more like a car (private good, you buy what you can afford).

The numbers and figures can tell you what each system costs and what outcomes it produces, but there are always tradeoffs, and that part is a moral choice.

And in a democracy, moral choices get made through politics, which is largely why this debate never fully resolves, and why people on both sides can look at the same evidence and reach completely different conclusions.

Don’t @ me, Mark Ruffalo.

Stay up.

j

go deeper

1. Find out how your insurer actually spends your premium — CMS publishes Medical Loss Ratio data by insurer and state. It shows exactly what percentage went to actual care vs. overhead and profit.

2. See how US provider costs compare to peer nations — The Peterson-KFF Health System Tracker is the cleanest primary source on the cost gap, broken down by procedure, country, and year.